About Mirus

Three angles

Mirus engages in activities involving all aspects of the debt portfolio and guarantee positions. But debt portfolios come in many shapes and sizes. So what exactly is a debt portfolio? A debt portfolio is a collection of loans extended in the B-to-B market to clients.

Our 3 distinctive approaches:

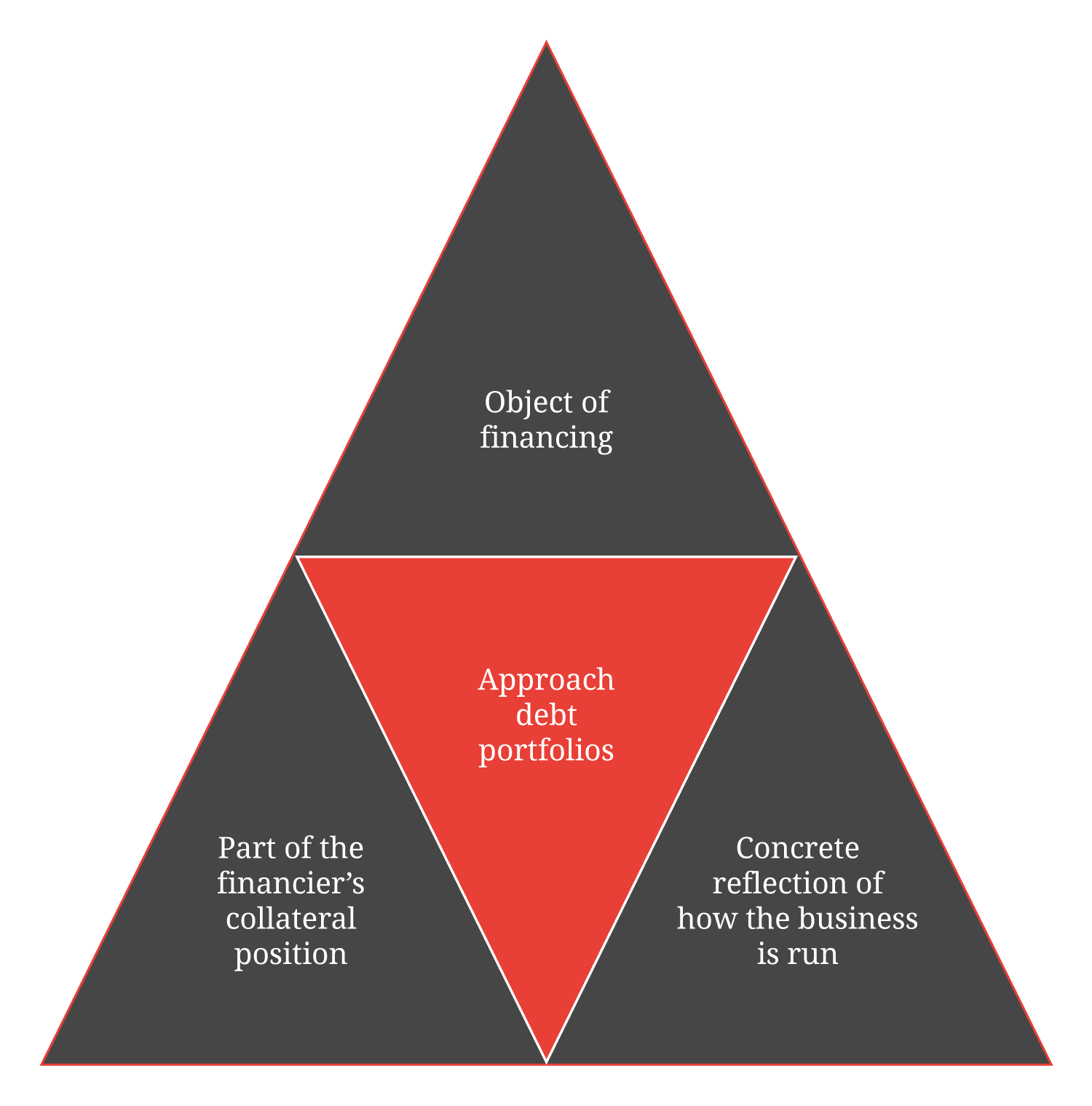

Debt portfolios as an object of financing: audit, valuation and advice

Debt portfolios as a concrete reflection of how the business is run

Debt portfolios as part of the financier’s collateral position: valuation and execution

Model

Specialisations

The three approaches are distinct but complementary specialisations.

Broadly speaking, a financial institution can finance a debt portfolio (asset based finance) in two ways:

1. factoring, which is invoice-based financing, and

2. borrowing base financing, which is based on the total portfolio and a number of corrections.

As an independent party Mirus can provide an opinion on the quality of the debt portfolio as part of asset-based financing. In this way, we can confirm or challenge the financial institution’s – or company’s – assessment of the company’s debt portfolio. During this process, insight is gained into the company’s procedures, its arrangements with clients and general business approach. Actions that the company takes when clients fail to meet their commitments are also taken into account, as are the internal procedures used when assessing new clients.

Depending on the client’s specific request, the final report will focus on a valuation of the debt portfolio – also in relation to the work in progress and (bank) guarantees issued in favour of third parties – and/or on advice to improve the intrinsic value of the debt portfolio.

Debt portfolios are packed with data at various levels: industry data and economic indicators at macro level; typology, changes in management, position in the supply chain, diversity of activities at creditor level (the company itself); current contracts, revenue data, degree of concentration, credit limits and credit insurance, consolidation issues and creditor positions at debtor level; credit amounts, inconsistent invoice numbers, number sequences, descriptions, codings at invoice level.

Databases, models and historical data make it possible to efficiently and effectively arrange and interpret data in a meaningful way. Questions may arise in specific sub-areas which can be resolved through algorithmic investigation. Mirus is continuously perfecting these tools to meet the market’s changing needs in order to generate relevant insights, insofar as technically possible. Hands-on debt collection generates data that is used as input for standard setting and this practice ensures that standard setting is constantly adjusted.

Ultimately, however, the models do not actually produce solutions. They establish order amid chaos and generate relevant questions. Answers to these questions are then sought by having interviews with the company’s financial and commercial officers. Their answers are translated into a concrete assessment of how the business is run, after which these findings are recorded in the contract records.

A multitude of subjects are addressed in this context, such as current guarantee obligations, bonus arrangements, Dutch Chain Liability (WKA) issues and delivery commitments. While the previous phase consisted of a structured statistical approach using databases and models, this phase centres on social interactive skills, legal knowledge and the human dimension.